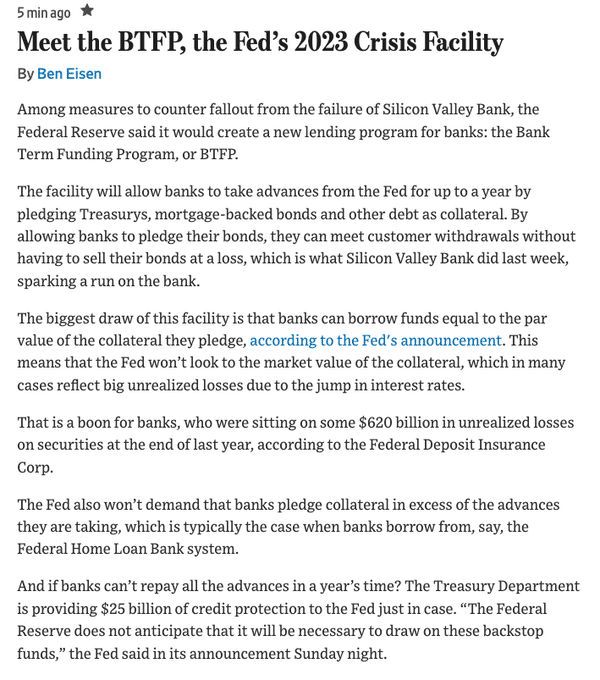

On Sunday afternoon, the Fed and Treasury rode the rescue with the Bank Term Funding program, BTFP, the latest bank bailout. The government staring at potential bank runs shored up banks and helped comfort depositors that their money is safe. The facility will save some banks from selling underwater bonds and taking losses in order to free up cash for depositors. Consequently, participating banks can pledge eligible bonds to the BTFP facility and receive a one-year loan for the bond’s par value. The facility only applies to U.S. banks and bonds owned before the announcement. Some banks may be unable to take advantage of the program as they do not hold a measurable amount of Treasuries or MBS. The BTFP program will last for one year.

Now, our two cents and what this means from a macroeconomic perspective. For starters, the Fed may have more leeway to raise rates as most banks are protected against being forced to take losses and raise capital. Counter to the argument, lending standards will increase significantly, which will drag on economic activity and do the Fed’s heavy lifting. Further, tightening standards will put those companies most heavily reliant on bank funding at risk. Some believe BTFP opens the door for a Fed pivot. With the battle against high inflation still in progress we are not sold the Fed will give up the fight so early. We will learn a lot more about the program at next week’s FOMC meeting.

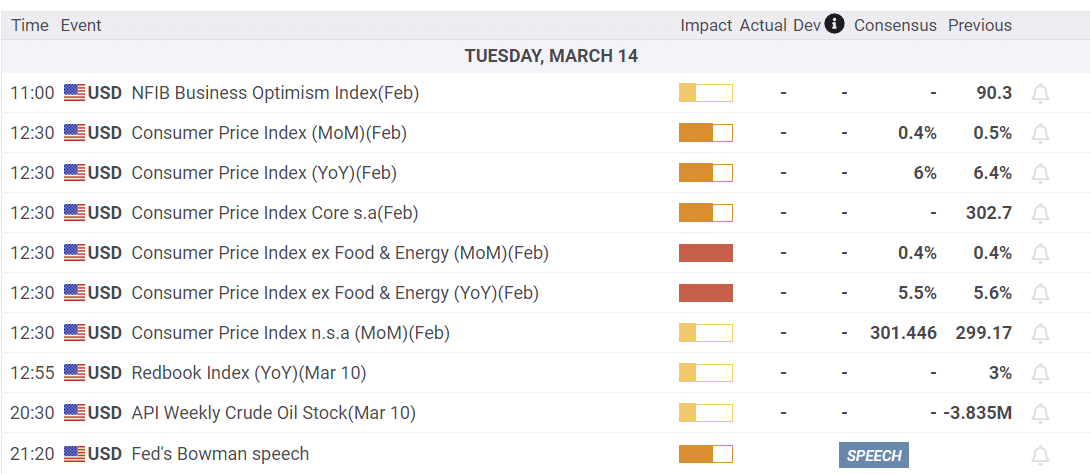

What To Watch Today

Economy

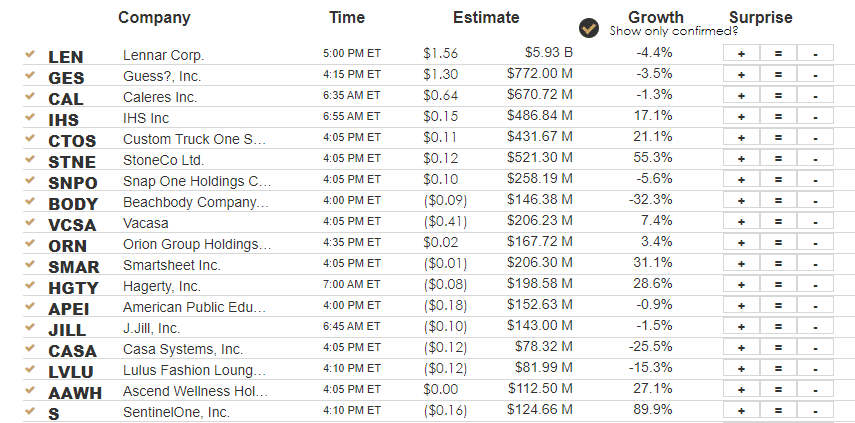

Earnings

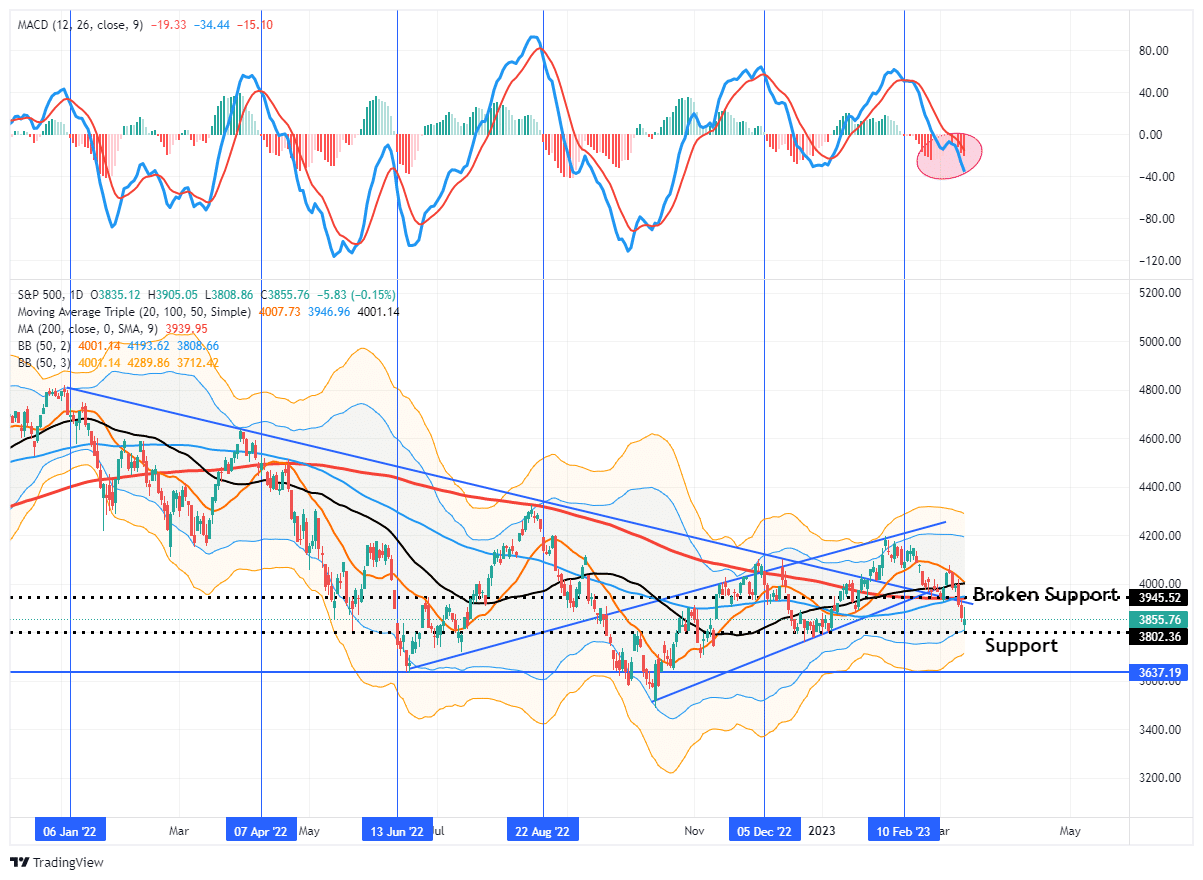

Market Trading Update

The market rebounded from the opening lows as the Fed launched a program allowing banks to provide discounted collateral for loans at full face value. This facility will allow banks the capital they need to meet depositors’ redemption requests. However, as discussed next, with more regional banks having trouble, the market rebound had trouble hanging on for the day.

The market is oversold but has broken all major supports of the previous bullish trend. Such puts us into “risk off” mode and suggests we use short-term rallies to reduce risk and rebalance portfolios. We have warned several times over the last year, that the aggressive rate hiking campaign would break something either in the economy or the credit market.

It appears the first cracks are in the credit market. Such is seen in the US sovereign credit risk based on 1Y CDS spreads, which have soared to a record high. This move eclipses what was seen during the Lehman event or the debt ceiling crisis.

Hold positions now as the market bounced off support from the December lows. However, use any reflexive rally that does NOT clear the 200-DMA as an opportunity to raise cash and reduce risk.

More Regional Banks on the Ropes

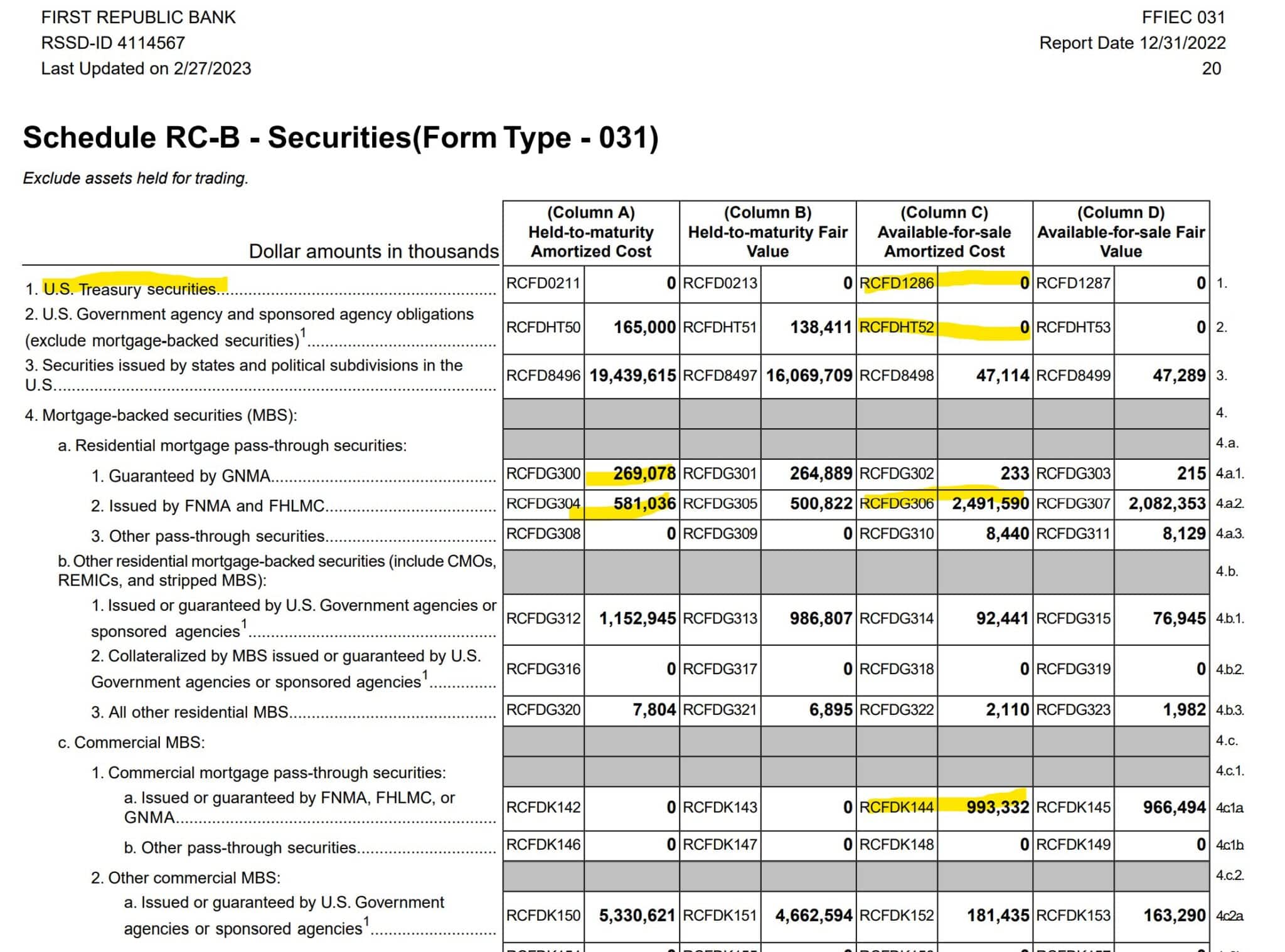

Despite the BTFP program, many regional bank stocks are still struggling. For instance, First Republic Bank (FRC) is down about 75% in just the last week. Joseph Wang, an ex-Fed employee, shows why the stock is sharply lower in Monday’s trading below. Most of FRC’s holdings are in municipal bonds. As of year-end, they held no Treasury securities and only a small amount of MBS or agency assets. As it is currently structured, BTFP will not help them avoid losses. We suspect investors are combing through bank balance sheets to figure out which banks can take advantage of the bailout. Some of those that can’t may join Silicon Valley Bank in receivership unless the Fed devises a new structure.

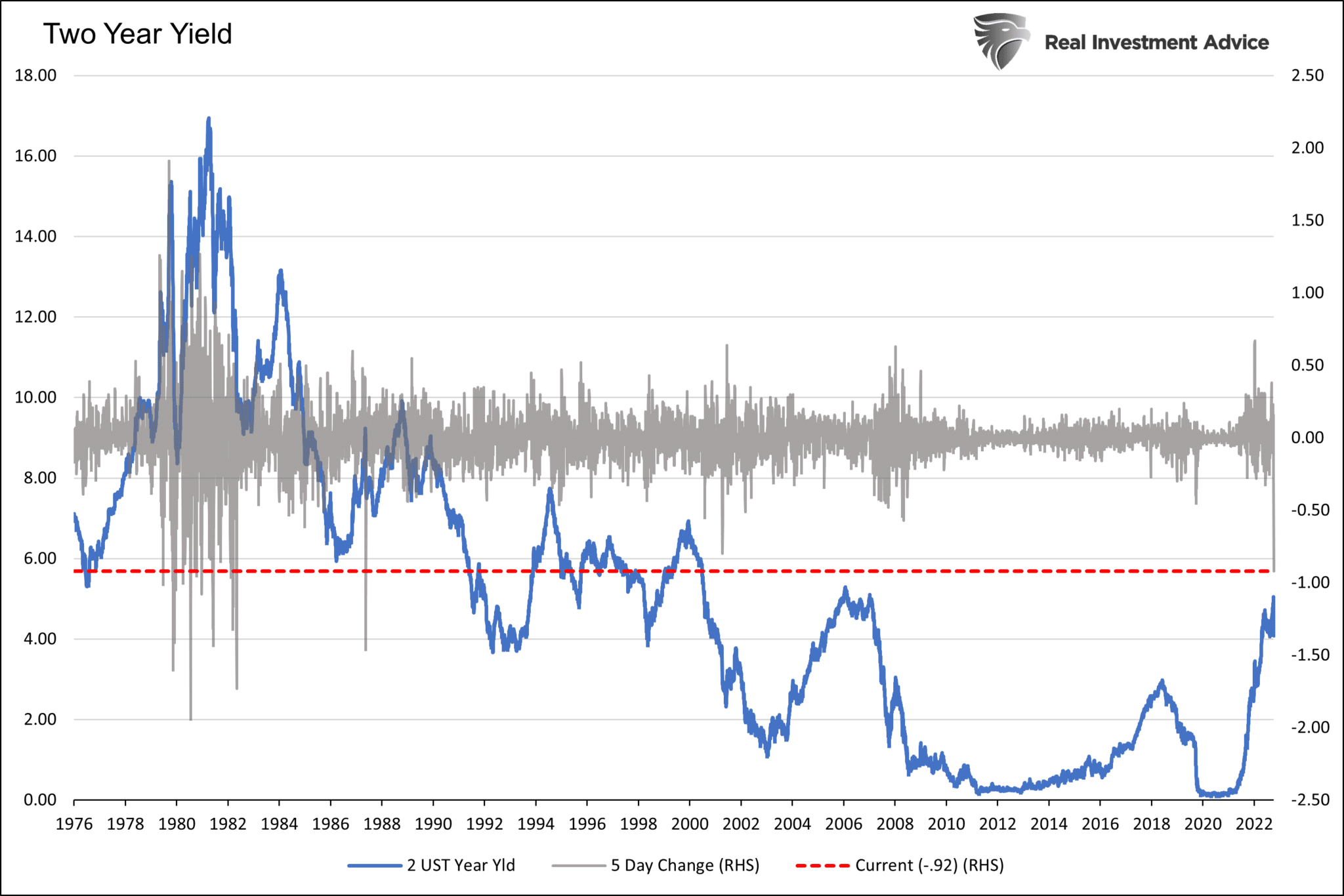

Two Year Yields Plummet

In just the last five days, the yield on 2-year Treasury notes has fallen nearly 1%. As the graph below shows, the last time it fell by as much in such a short period was 1988. The two-year yield is clearly pricing in a Fed pivot. Bond investors now assume that the Fed will prioritize the banking sector over inflation. If that proves true, the cessation of rate hikes, possibly after the March meeting, and a pivot are probable. That said, if the Fed thinks they have properly protected banks from more losses due to higher interest rates, the two-year yield may reverse recent gains.

Places to Hide in the Financial Sector

Within we share our proprietary relative and absolute analysis on markets, sectors, factors, and stocks. The analysis uses 13 technical studies to assess which stocks are over or underperforming versus the market, its sector, or on a stand-alone basis. Today we share our analysis and dive into the financial sector and see which stocks are holding up well despite the turmoil.

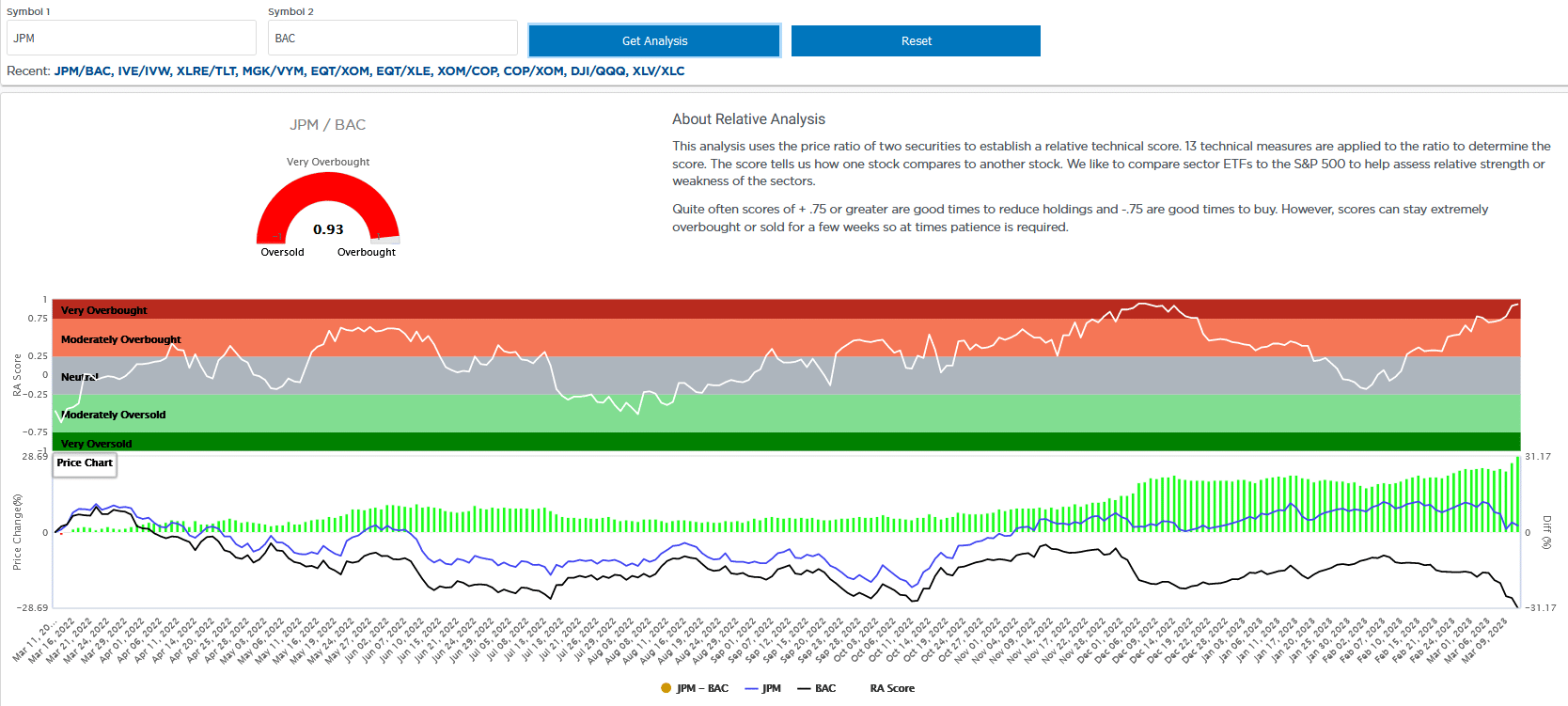

The table below shows how the top ten holdings of XLF score relative to XLF. Our relative analysis uses technical analysis on the price ratio of each stock to XLF and assigns a score. The higher the score, the more overbought the stock is compared to XLF. Conversely, lower scores are those that are oversold. As shown, JPM is the most overbought bank in the financial sector. Bank of America (BAC) is the most oversold. Often highly overbought or oversold conditions normalize.

The second graphic is a relative comparison of JPM to BAC. Not surprisingly, the ratio is extremely overbought (in JPM’s favor). If you think the banking crisis is ebbing, you may want to dip your toes in the most underperforming stocks, like BAC. That said, there are many unknowns, and we advise prudence and, as such, staying away from banking stocks until the smoke clears a bit.

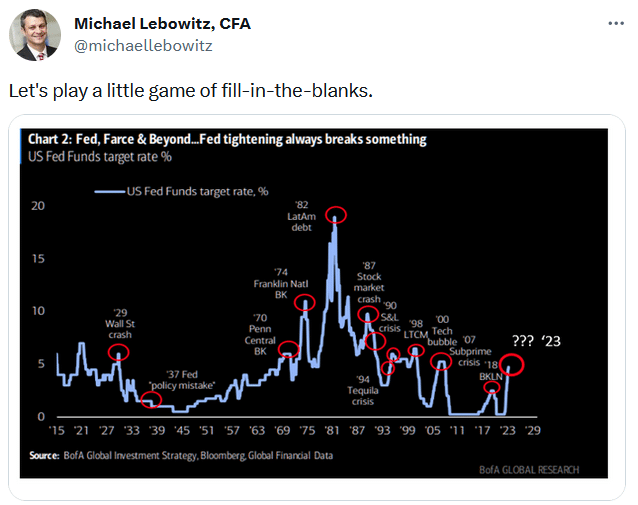

Tweet of the Day

Please to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.